The state of alarm has modified the deadlines established for the legalization of the books and the deposit of the Annual Accounts for the 2019 financial year.

The contradictions and revisions in all types of decisions that COVID 19 is causing affect all economic and social areas and accounting matters could not be less. In this sense, Royal Decree-Law 19/2020 comes to “modify” what is regulated in Royal Decree-Law 8/2020 referring to the formulation, approval and deposit of the Annual Accounts.

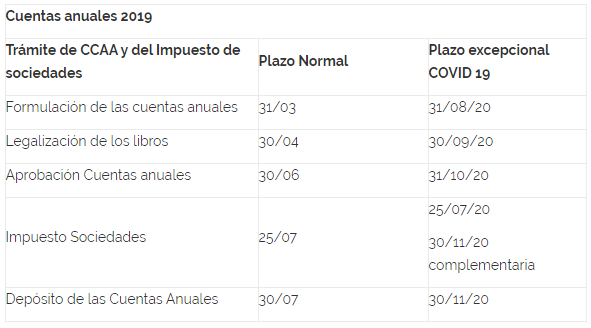

Perhaps because the situation is taking longer than expected, the new regulations dissociate the end of the state of alarm from the resumption of corporate deadlines suspended by RDL 8/2020, of March 17. As a consequence, it is established that the three-month period to prepare the annual accounts and other mandatory documents will begin to be counted from June 1, 2020 and not from the end of the state of alarm (which is unknown when it will arrive). The deadline for the formulation of the Annual Accounts will be next August 31.

Furthermore, although it is not expressly considered in the new rule, June 1 also begins the four-month period for the legalization of books.

Final calendar

The definitive calendar established in RDL 19/2020 and only exceptionally for the 2019 financial year leaves us with the following deadlines:

- Formulation of annual accounts

The annual accounts will be formulated within a period of three months from June 1, 2020. Therefore, the deadline for the formulation of the Annual Accounts is August 31, 2020. - Book legalization

The legalization of books will be done within a period of 4 months also from June 1, with its deadline therefore being September 30, 2020. - Account approval

The period for holding the Ordinary General Meeting for the approval of the accounts and the proposal for the distribution of the results is reduced from three months to two, so it must meet within the following two months from the end of the year. deadline for the formulation of the annual accounts. Ultimately, the deadline for approval of the 2019 annual accounts will end on October 31, 2020. - Presentation and deposit of annual accounts

The deadline for the presentation and deposit of the Annual Accounts in the Commercial Registry will be one month from their approval, so if the Ordinary Meeting approves the accounts on October 31, this must be done before November 30, 2020.

Corporation tax

The Treasury will allow the presentation of the normal self-assessment of Corporate Tax without prior approval of the accounts by the partners. Therefore, the usual deadline of July 25 is not modified. Of course, a second self-assessment of the tax will be allowed before the end of November, when the company has been able to definitively approve the accounts.

In summary, these will be the dates to take into account:

Ordinary deadlines

Because the declaration of the State of Alarm was made on a date very close to the deadline for the preparation of accounts, it is possible that many companies already had them formulated or at least prepared. In this sense, we must remember that this exceptional calendar for the year 2019 does not prevent those companies that deem it appropriate from preparing the Annual Accounts during the State of Alarm and legalizing the books and depositing them in the Commercial Registry in the ordinary term.

Results distribution proposal

Continuing with the previous idea, it is possible that companies that have prepared the annual accounts before the declaration of the state of alarm or during it, included a proposal for the distribution of results in their already closed report that, however, due to to subsequent events, understand that now it is not the most accurate.

In this sense, the College of Registrars and the National Securities Market Commission have issued a joint statement giving the possibility of changing the proposal for the distribution of results formulated based on various circumstances.

We see that, despite not yet being in the so-called “new normal”, it is true that some commercial and fiscal aspects are being tried to normalize, even if it is on different dates than what we are used to. It is advisable to take note of them in order to avoid disappointment.

Source: INEAF